What is Peer to Peer lending (P2P)? How far the recent regulation of P2P by RBI will influence the credit discipline in India?

Refer - Business Line

IAS Parliament 6 years

KEY POINTS

Peer to Peer Lending

· P2P companies provide a platform or market for borrowers and lenders.

· P2P lending ideally refers to unsecured lending mostly happens on online platforms, outside of the parameters of banks or non-banking finance companies.

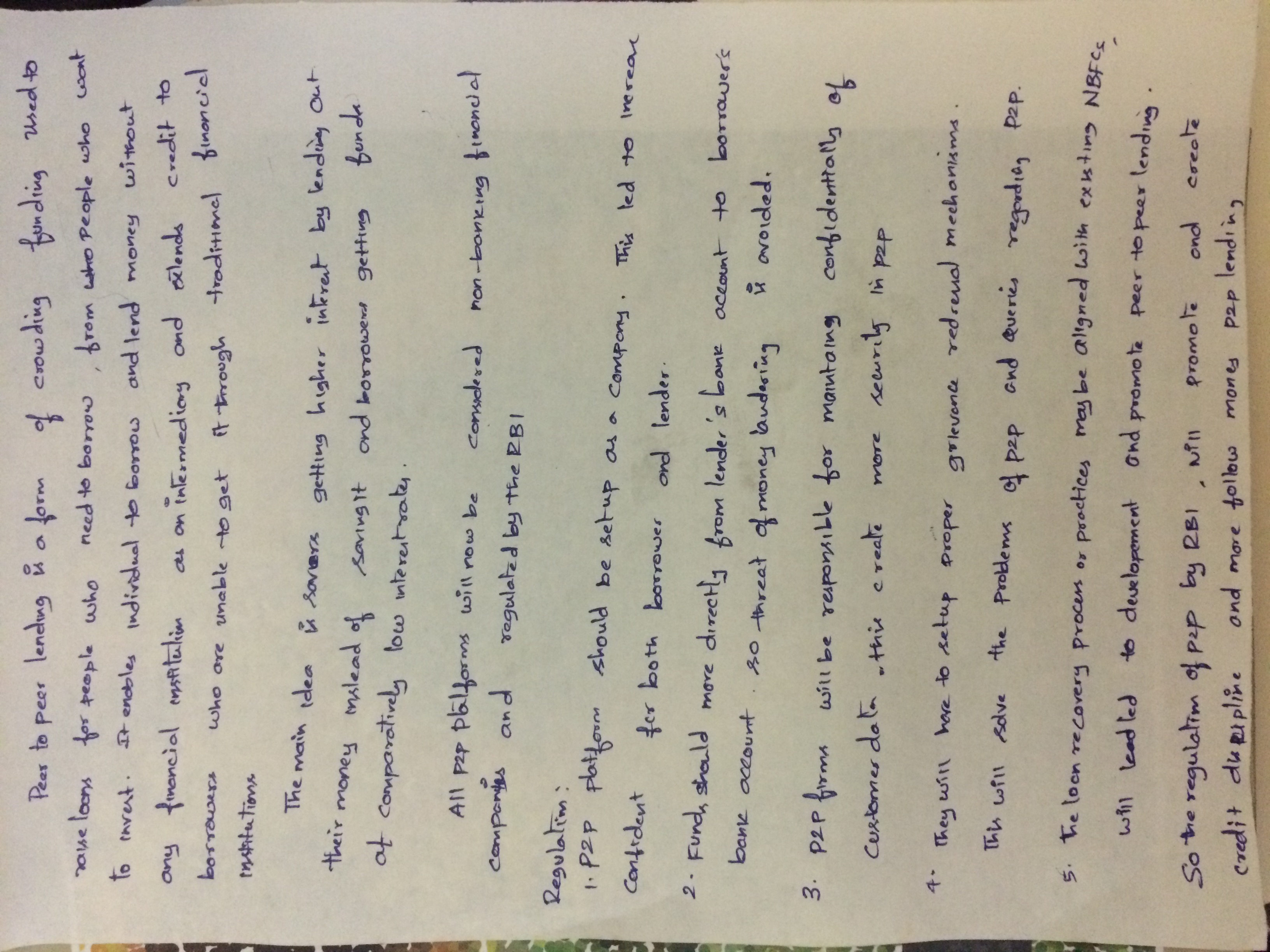

RBI Regulation

· RBI had recently declared that, all peer-to-peer lending (P2P) platforms would be treated hereafter as non-banking financial companies (NBFCs) and will be regulated by the Reserve Bank of India (RBI).

· RBI had also released guidelines to regulate NBFC – P2P.

· Hitherto, wary of an unregulated marketplace the RBI has cleared the way for more investors to join the fray.

· Apart from lending, a helping hand to the Centre’s financial inclusion drive by providing easy access to credit.

· RBI’s directives will also ensure that only serious playersable to comply with the norms, stay in the game.

· The clarification that an NBFC-P2P can act only as an intermediary, facilitating lending activity, and not take deposits or lend on its own, spares such platforms of the burden of provisioning or capital adequacy.

· It also helps avoid conflict of interest which could have risen if P2P platforms were allowed to use their own funds for on-lending.

· The guidelines also require P2Ps to become members of credit information companies and maintain and update credit information of the borrower.

· This should help mitigate risk of defaults, attract investments and drive innovations.

Unaddressed issues

· The blanket cap of 10 lakh on a lender’s exposure across all platforms can repress flows.

· The cap of 50,000 on exposure of a single lender to the same borrower serves the purpose of mitigating the risk of default, the regulator can remove or increase the cap on a lender’s aggregate exposure.

· Many P2P platforms have been employing agents to offer recovery services.

· While the RBI has cautioned P2P platforms against the use of coercion, there is still lack of clarity among players on their legal rights when proceeding against borrowers.

jerry 7 years

peer to peer lending