Click here for Part II and here for Part I

Why in news?

The Union Minister for Finance and Corporate Affairs, Ms. Nirmala Sitharaman tabled the Economic Survey 2018-19 in the Parliament.

What are the key highlights?

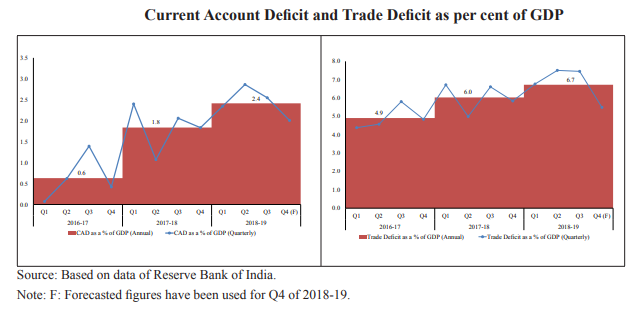

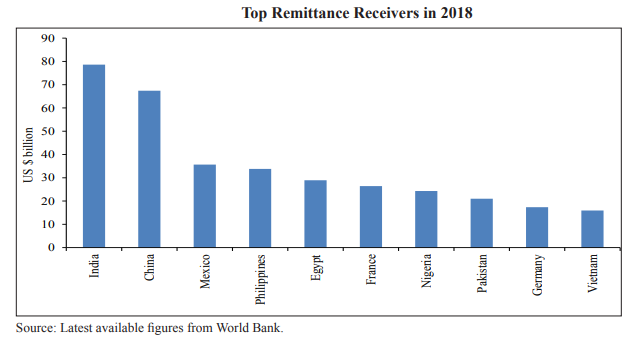

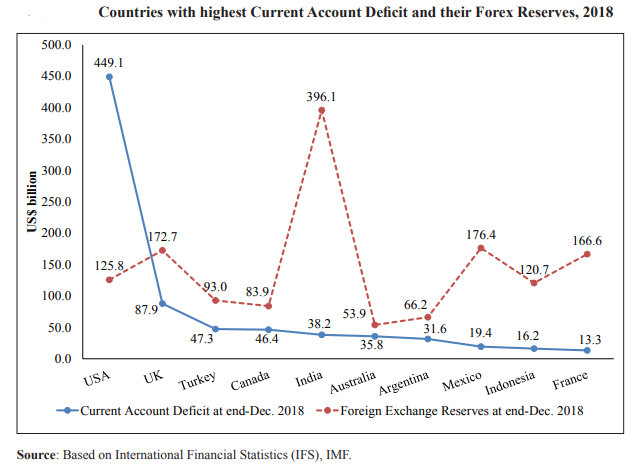

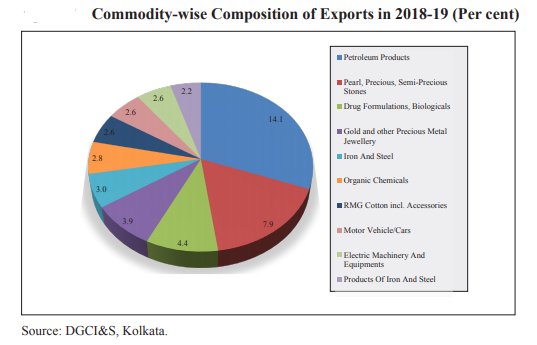

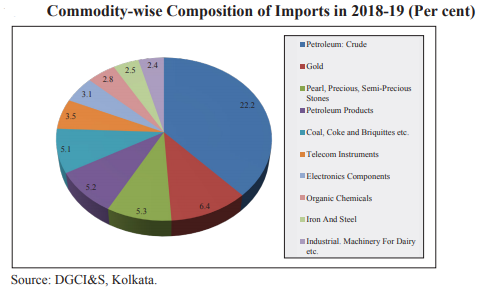

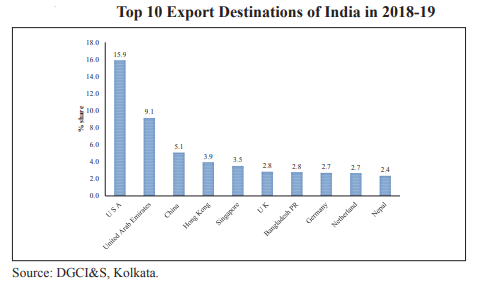

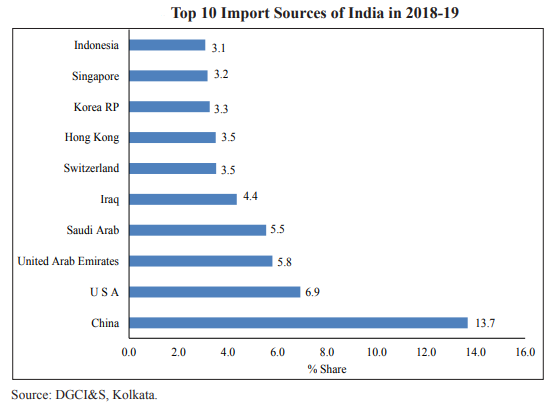

EXTERNAL SECTOR

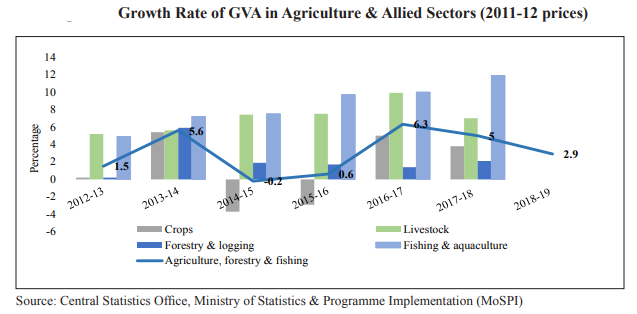

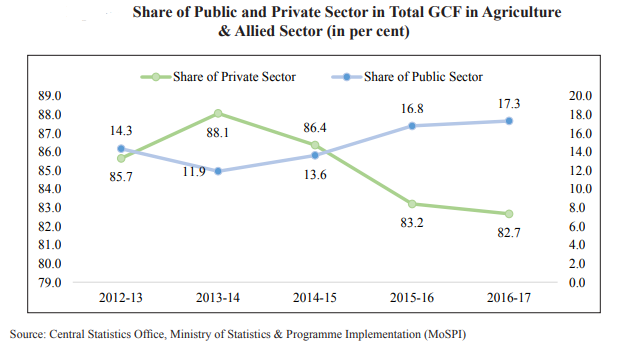

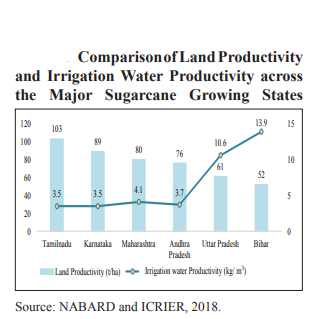

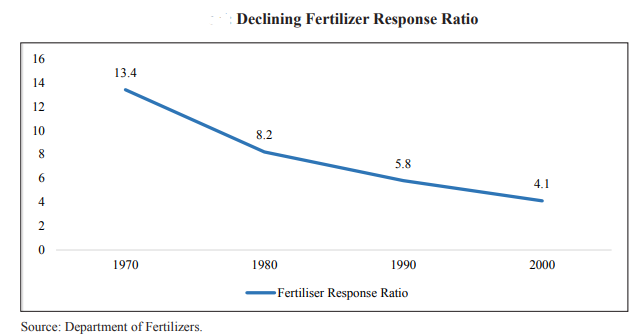

AGRICULTURE AND FOOD MANAGEMENT

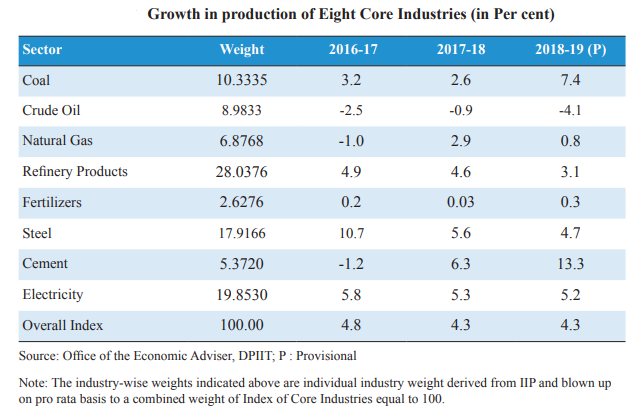

INDUSTRY

INFRASTRUCTURE

SERVICES SECTOR

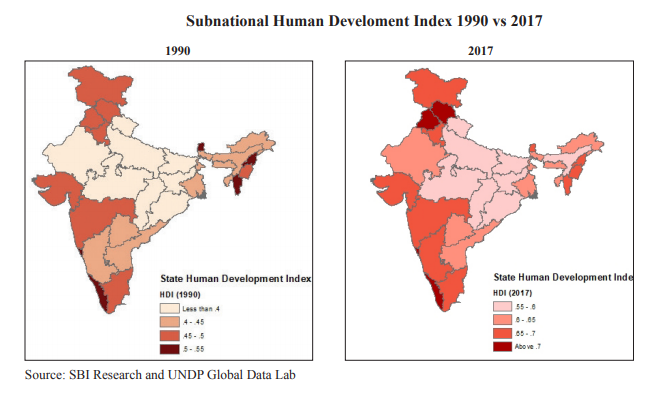

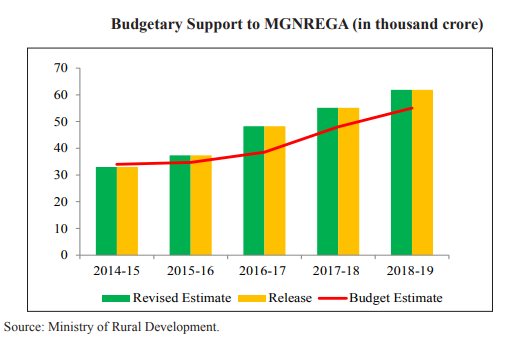

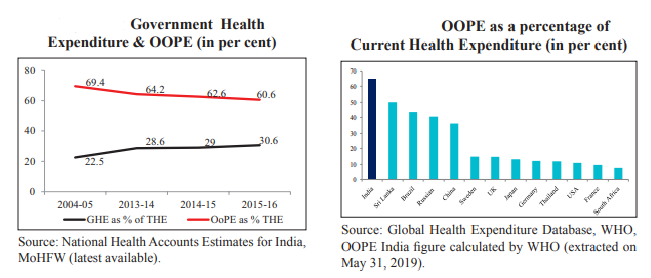

SOCIAL INFRASTRUCTURE, EMPLOYMENT AND HUMAN DEVELOPMENT

Note: OOPE - Out of Pocket Expenditure; THE - Total Health Expenditure

Source: Ministry of Finance Website