The Reserve Bank of India has recently launched the e-Rupee for retail users.

What is e-Rupee?

It is an electronic version of cash in the form of a digital token.

It is the Central Bank Digital Currency (CBDC) issued by the Reserve Bank of India (RBI).

It will be primarily meant for retail transactions.

Earlier in November 2022, the RBI launched the digital rupee for the wholesale segment to settle secondary market transactions in government securities.

Wholesale CBDC is designed for restricted access to select financial institutions.

On the other hand, Retail e-rupee can be potentially used by all — the private sector, non-financial consumers and businesses and provide access to safe money for payment and settlements.

CBDC will appear as ‘liability’ (currency in circulation) on the RBI’s balance sheet.

How it works?

It is a fungible legal tender, for which holders need not have a bank account.

E-rupee will be issued in the same denominations as paper currency and coins, and will be distributed through the intermediaries, that is banks.

Transactions will be through a digital wallet offered by the participating banks, and stored on mobile phones and devices.

Transactions can be both person to person (P2P) and person to merchant (P2M).

A user will be able to withdraw digital tokens from banks in the same way she can currently withdraw physical cash.

She will be able to keep her digital tokens in the wallet, and spend them online or in person, or transfer them via an app.

Who can use the retail CBDC?

The first phase of the CBDC will cover Mumbai, New Delhi, Bengaluru and Bhubaneswar.

Participating banks include State Bank of India, ICICI Bank, Yes Bank, and IDFC First Bank.

Subsequently, the service will be extended to other cities and banks.

Offline Transactions - There is no indication yet from the RBI that the e-rupee will function in the offline mode.

A risk of ‘double-spending’ exists in offline mode — because it will be technically possible to use a CBDC unit more than once without updating the common ledger of CBDC.

How e-rupee is different from the cryptocurrency?

CBDC is backed by the RBI whereas crypto currencies are private virtual currencies like Bitcoins that have no issuer.

In fact, the RBI wants the government to ban cryptocurrencies in India.

Private virtual currencies are not commodities or claims on commodities as they have no intrinsic value.

The inherent design of cryptocurrencies is to bypass the established intermediation that ensures integrity and stability of the monetary and financial ecosystem.

How e-rupee is different from UPI transacted digital money?

Intermediaries - For money transfer in UPI payment system, one needs to make a request and forward it to the account holder’s bank.

The bank then decides to deduct the balance and transfer it to the beneficiary account.

So, there’s a chain of intermediaries who enable this transaction.

However, e-rupee did not need any intermediaries at all and it requires transfer of digital money from one’s wallet to another wallet.

Transaction limit - UPI-based apps like Google Pay and Paytm have a daily and per-transaction spending limit.

But the RBI has not fixed any limit on holding digital rupees in wallets.

Digital rupee transactions above Rs 2 lakh are likely to be reported for tax matters.

What are the benefits of e-rupee?

CBDC has the potential to provide significant benefits such as:

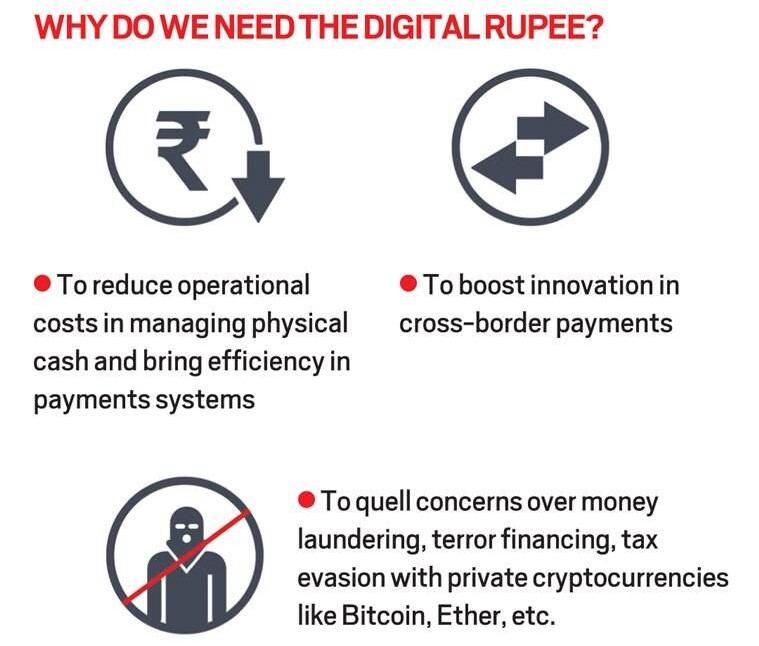

Physical cash - It reduces the dependency on cash.

Seigniorage - Higher seigniorage due to lower cost of printing, transporting, storing and distributing.

(seigniorage - The difference between the face value of money and the cost to produce it)

Settlement Risks - Payments are final, and thus reduce settlement risk in the financial system.

Interbank Settlement - When CBDC is transacted instead of bank balances, the need for interbank settlement disappears.

Universal payment systems - CBDC can also enable a more real-time and cost-effective globalization of payment systems.

Risks of crypto currency - The risks associated with the private cryptocurrencies like Bitcoin, Ether, etc. such as money laundering, terror financing, tax evasion can be overcome by the RBI regulated CBDC.

Other benefits

Fostering financial inclusion

Bringing resilience, efficiency and innovation in the payments system.