The RBI recently gave license to National Asset Reconstruction Company Limited (NARCL), popularly known as a bad bank but the absence of a clause about the lifespan of NARCL may lead to a moral hazard problem.

What are bad banks?

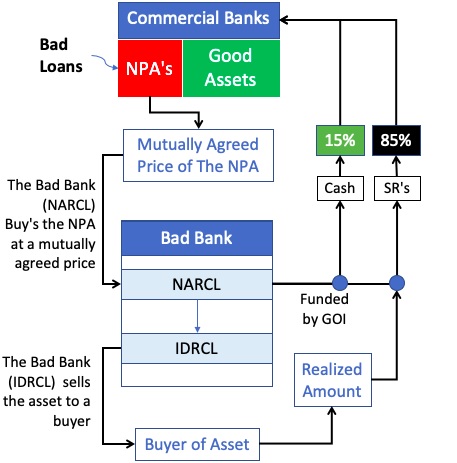

Technically, a bad bank is an asset reconstruction company (ARC) or an asset management company that takes over the bad loans of commercial banks, manages them and finally recovers the money over a period of time.

The bad bank is not involved in lending and taking deposits.

It just helps commercial banks clean up their balance sheets and resolve bad loans.

The takeover of bad loans is normally below the book value of the loan and the bad bank tries to recover as much as possible subsequently.

US-based Mellon Bank created the first bad bank in 1988.

The role of the bad bank is to establish a liquid market for NPAs to enable the banks to sell their NPAs at a fair value.

What is the status of NPAs in India?

Currently, the Indian banking system has one of the highest gross non-performing assets (GNPA) to total asset ratio globally.

Post-covid stress scenarios estimated by the RBI pegs it at an aggregate GNPA ratio in the range of 12.5- 14.7 %

What mechanisms have been initiated to recover NPAs?

Debt recovery tribunals - under the Recovery of Debts Due to Banks and Financial Institutions (RDDBFI) Act in 1993

Asset Reconstruction Companies (ARCs) - a part of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act (SARFAESI Act) in 2002

Insolvency and Bankruptcy Code (IBC) in 2016

What is NARCL?

India’s first-ever bad bank, National Asset Reconstruction Company Limited (NARCL) will acquire stressed assets worth about Rs 2 lakh crore from various commercial banks

It will pay 15% of the agreed price in cash and the remaining 85% will be in the form of Security Receipts.

The rest will be paid when the assets are sold by India Debt Resolution Company Ltd (IDRCL).

Rs 90,000 crore of the asset will be managed in the first phase.

A government guarantee will back the Security Receipts for a maximum amount of Rs.30,600 crore, and the guarantee will be valid for a resolution period of five years.

The NARCL is essentially an Asset Reconstruction Company (ARC) with only two distinguishing features

NARCL is intended for dealing in big sized tickets

NARCL has a partial government guarantee.

The effectiveness of ARCs hinges on

A focused mandate for setting up the ARCs

Limited lifespan of the ARC

Market-based resolution of NPAs

What are the issues in NARCL?

The absence of a clause about the lifespan of NARCL may lead to a moral hazard problem.

Propagation and evergreening of bad loans - Public sector banks (PSBs) which own 51 % stake in NARCL may continue buying their own stressed assets through NARCL.

There are question marks over the government guarantee of Rs 30,600 crore in providing liquidity and creating a market for the NPAs.

How can the problems be addressed?

The government should address the lifespan issue of NARCL in the form of a sunset clause to increase the effectiveness of the NARCL.

There should be a fair and transparent mechanism while setting the haircut on the stressed assets by the NARCL.

The net asset value of the Security Receipts must be fairly priced to boost the participation and liquidity in the security receipts market.

There needs to be a strong political will to recognise bad loans and support legal infrastructure to address wilful defaulters.